Butterfly Spread Options Trading Strategy: In-Depth-Guide

Welcome to Dronakul options tutorial, in this Options Trading Course I will guide on the Butterfly Spread options trading strategy. Whether you're a novice or an experienced trader, mastering the Butterfly Spread can significantly enhance your trading portfolio. This advanced options trading strategy, including the Long Call Butterfly, Long Put Butterfly, Short Call Butterfly, Short Put Butterfly and Iron Butterfly, is designed to profit from low volatility in the underlying asset. In this article, I'll explain how to trade butterfly spread options, providing step-by-step insights and practical examples. By understanding the nuances of these strategies, you'll be well-equipped to capitalize on market conditions and optimize your trading outcomes.

Butterfly Spread Options Trading Strategy

The butterfly spread is an advanced options strategy that combines elements of both bullish and bearish spreads, allowing traders to profit from low volatility in the underlying asset. It involves multiple strike prices and generally requires four options contracts.

(Buy 1 lot ITM Call + Sell 2 Lots ATM Call + Buy 1 lot OTM Call Options)

(Sell 1 lot ITM Call + Buy 2 Lots ATM Call + Sell 1 lot OTM Call Options)

(Buy 1 lot ITM Put + Sell 2 Lots ATM Put + Buy 1 lot OTM Put Options)

(Sell 1 lot ITM Put + Buy 2 Lots ATM Put + Sell 1 lot OTM Put Options)

(Sell 1 lot ATM Call + Buy 1 Lot OTM Call) + (Sell 1 lot ATM Put + Buy 1 lot OTM Put)

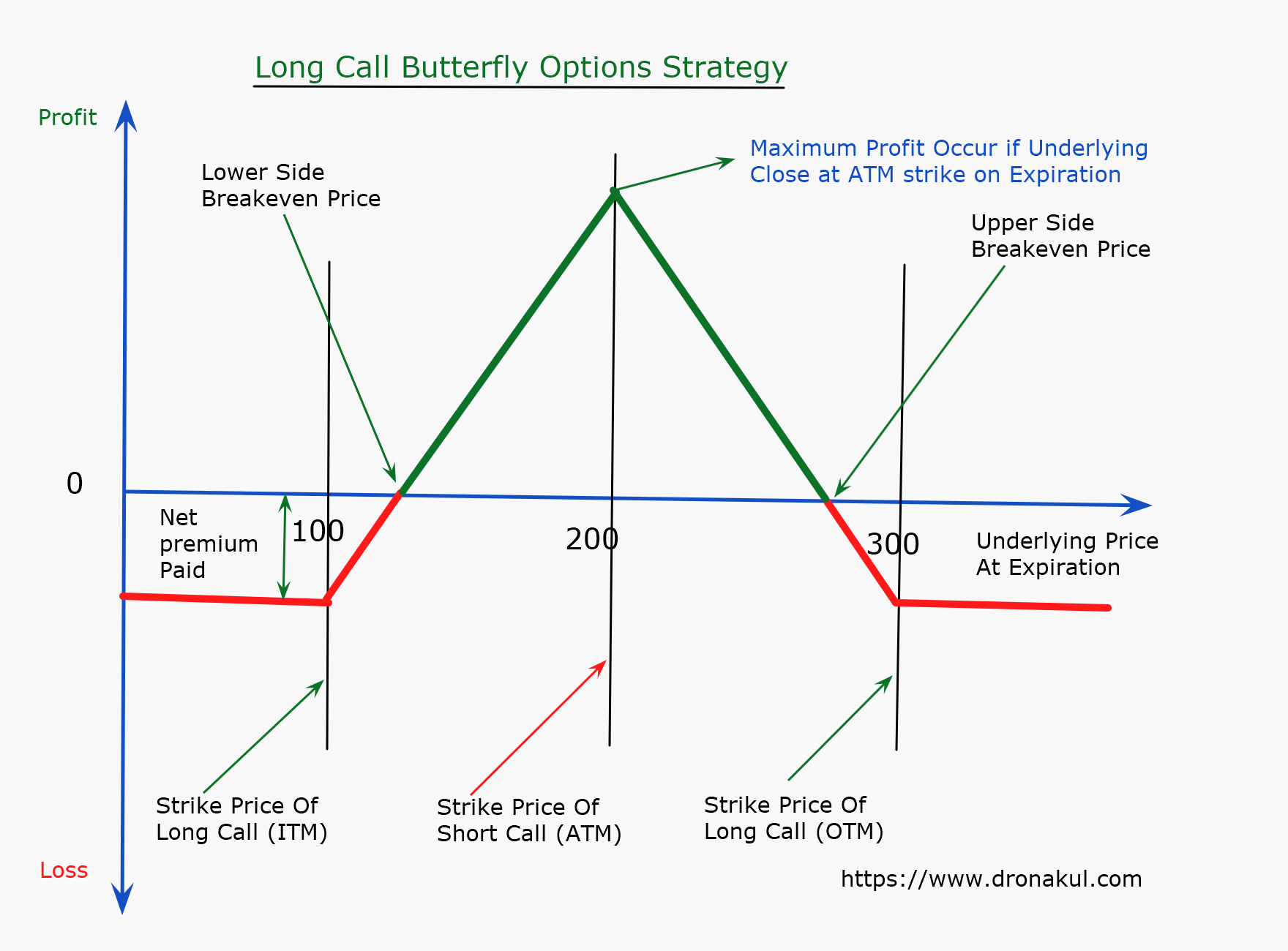

Long Call Butterfly Options Trading Strategy

Long call butterfly is a combination of a Bull Call Debit Spread and a Bear Call Credit Spread to make profit from low volatility or narrow range trading of the underlying.

Trade Construction:

Buy 1 In-The-Money (ITM) call option

Sell 2 At-The-Money (ATM) call options

Buy 1 Out-Of-The-Money (OTM) call option

Ideal Market Outlook:

Neutral or slightly bullish, expecting the stock price to stay within a range. Benefits from time value decay (loss of value in options as expiration approaches) if the price remains near the center ( ATM).

Profit Potential: Limited

Maximum Profit:

Achieved if the underlying stock price stays near the ATM strike price (price of the sold calls) at expiration. Profit is equal to the difference between the strike prices of the long and sold calls minus premiums paid. It means, if we select strike price little deep ITM and Far OTM for buying call options, then the profit potential will increase, we need to remember that risk will also increase in that case.

Risk: Limited to the premium paid for the spread.

Breakeven Prices:

This is the price at which the underlying asset needs to be at expiration for the spread to break even means, neither you gain nor you lose money.There are two breakeven prices for a long call butterfly

Lower Breakeven Price:

Lower Breakeven = Lower Strike Price + Net Premium Paid

Lower Strike Price: This is the strike price of the in-the-money (ITM) call option you bought in the spread.

Net Debit Paid: This is the total cost of the spread, which is the difference between the premium paid to buy the ITM and OTM calls and the premium received from selling the two ATM calls.

Upper Breakeven Point:

Upper Breakeven = Upper Strike Price - Net Premium Paid

Upper Strike Price: This is the strike price of the out-of-the-money (OTM) call option you bought in the spread.

Net Debit Paid: Same as above, the total cost of the spread.

Example:

Assume Nifty Trading at 24568, So 24550 is the ATM call option

We can Buy 24500CE 1 lot, sell 24550CE 2 lots and Buy 24600CE 1 lot (Building the strategy without any strike gap).

Or we can buy 24450CE 1 lot, Sell 24550CE 2 lots and buy 24650CE 1 lot (Building the strategy with 1 strike gap).

See the picture right side for the Nifty Options prices ready reference on 22 July 2024, it was a live market screenshot around 11:00 a.m. Now see the mechanics of long call butterfly.

Buy 1 lot 24500CE at 256...... Premium Paid = 256.00

Sell 2 lots 24550CE at 229..... Premium Received = 2*229=458.00

Buy 1 lot 24600CE at 204...... Premium Paid = 204

___________________________________________________________________

Total Premium Paid = 256+204 = 460

Total Premium Received = 458

Net Premium Paid = (460 -458) = 2.00

For learning purpose lets learn how to calculate if the strategy build without any strike price gap ..

Assume Nifty will expire at lower strike price 24500, on expiry

Premium of Nifty 24500CE will be 0 (Zero), We will book loss ₹256.00

Premium of Nifty 24550CE will be 0 (Zero), We will book Profit ₹229*2=₹458.00

Premium of Nifty 24600CE will be 0 (Zero), we will book loss ₹204.00

Profit / Loss = 458.00 -460.00

= -2.00

Even if Nifty fall far below 24500, all the options will become 0 and our maximum loss will be only ₹2.00 (Currently Nifty lot size is 25 so total loss will be 25*2=₹50.00). This will be our maximum loss.

Now Assume Nifty will expire at higher strike price 24600 on expiry.

Premium of Nifty 24500CE will be 100 , We will book loss ₹156.00

Premium of Nifty 24550CE will be 50, We will book Profit ₹(229-50)*2=₹358.00

Premium of Nifty 24600CE will be 0 (Zero), we will book loss ₹204.00

Profit / Loss = 358.00- 360.00

= - 2.00

If Nifty rises above 24600, then 24550CE will give us loss ₹2.00 for every 1 point up in the Nifty wehere 24500CE & 24600CE each will give ₹1.00 profit for 1 point up in the Nifty. Mean even if Nifty move up far above 24600, we can't lose more than ₹2*lot size

So we can say our loss is very limited. Practical established the theory.

Maximum Loss = net Premium Paid

Now assume Nifty will expire at 24550 (Middle strike price or ATM)

Premium of Nifty 24500CE will be 50 , We will book loss ₹206.00

Premium of Nifty 24550CE will be 0, We will book Profit ₹229*2=₹458.00

Premium of Nifty 24600CE will be 0, we will book loss ₹204.00

In this case profit for sold call options is ₹458.00 where loss for long call options is ₹410.00, our maximum profit will be ₹48.00*lot size. We will be in profit if Nifty close between upper and lower breakeven price on expiry.

So the formula of Maximum Profit = Strike Difference Between Traded ATM & ITM - Net Premium Paid

The Nifty can close anywhere in between Upper and lower breakeven price, then what will be the profit calculation?

We have already seen if the underlying expire at sold call options strike price we will gain maximum profit. It means if the underlyign move up or down from the middle strike price (sold call options strike price) our profit will reduce gradually and at breakeven point it will be 0 (Zero).

Here If Nifty fall below 24550, then we will lose ₹1.00 in 24500CE for every 1 point delcline where there will be no gain from 24550CE as it has already become zero. Oppositely, we will lose ₹2.00 from 24550CE for every 1 point up move in Nifty (As sold 2 lots) and gain only ₹1.00 from 24500CE but no gain or loss from 24600CE

For example if Nifty expire at 24570 then profit = 48 -20=28 (20 comes from LTP - Middle Strike)

if Nifty expire at 24542 then profit = 48 - 8 =40 (8 Comes from Middle Strike - LTP)

So the formula of Profit will be like this

Profit = Maximum Profit - Difference Between Sold Call Options Strike & Underlying Price LTP

= (Strike Difference Between Traded ATM & ITM - Net Premium Paid) - Difference Between Sold Call Options Strike & Underlying Price LTP (Where LTP refers the closing price of the underlying on expiry)

Long Call Butterfly Strategy Buildup With Strike Price Gap

As I mentioned earlier that profit potential is very low in this strategy, we may find out some way to increase profit potentiol also. Yes we can adjust with strike price by giving even or uneven gap to select the strike price. Lets see example.

Buy 1 lot Nifty 24450CE at 284, premium paid ₹284.00

Sell 2 lots Nifty 24550CE at 229, Premium Received ₹458.00

Buy 1 lot Nifty 24650Ce at 181, Premium paid ₹181

______________________________________________________________________

Net Premium Paid= ₹(284+181)-458

= ₹7.00

Either side big movement will cause a maximum loss of ₹7.00 * lot size only.

Maximum Profit = Difference Between Traded ITM & ATM - Net Premium paid

=(24550-24450) -7

= 100-7

=93

If Nifty expire at middle strike price, we will abale to make more profit than previous butterfly strategy. To maximize the profit potential we can trade with more strike price gap, but we need to remember the margin required for the strategy will also increase, risk will also increase slightly.

Timing, underlying selection and volatility are the most important factors for long call butterfly options trading strategy. Let me explain both.

Volatility:

Long call butterfly is more effective when market volatility is less than the normal, a continuous monitoring of options chain of the underlying is important and need to maintain the data. Always focus on ATM call and put options Implied Volatility (Implied volatility measures based on Options Prices, it is a measure of the market's view or prediction for the future volatility. It responds to crowd psychology and can reach unreasonable extremes. Instantaneous.) In a range bound scenario the strategy work better.

Timing:

Once the impact of any event in the underlying or market is over is best time for Long call butterfly. Normally what happen, after the event impact market or underlying moves very slowly but still the time value (Time value is the amount options buyers pay to the seller over and above the intrinsic value in options premium, ATM and OTM options consist only Time value.) remain higher.

Underlying Selection:

Index options are better due to availability of weekly expiry, as within less time result of the strategy comes out. Where monthly expiry options are hectic for long call butterfly. Besides the Index options has much more liquidity and less fear of huge gap up or gap down opening during the strategy period.

Preference Of Strike Selection:

For shorting, ATM call options is fixed for long call butterfly, but the strike gap selection is tricky. I first check what will be my premium receive amount for selling 2 lots call options and then decide which ITM and OTM call to buy. For example, assume I sold 2 lots Nifty 24500CE at 229, so I received a premium of ₹458.00, I will look for an ITM strike which is trading in between ₹420-430 and an OTM which is trading around ₹50-60, in that case I will be in profit even if the range is big, and if remain in small range bound then maximum profit will be far better than other strategy.

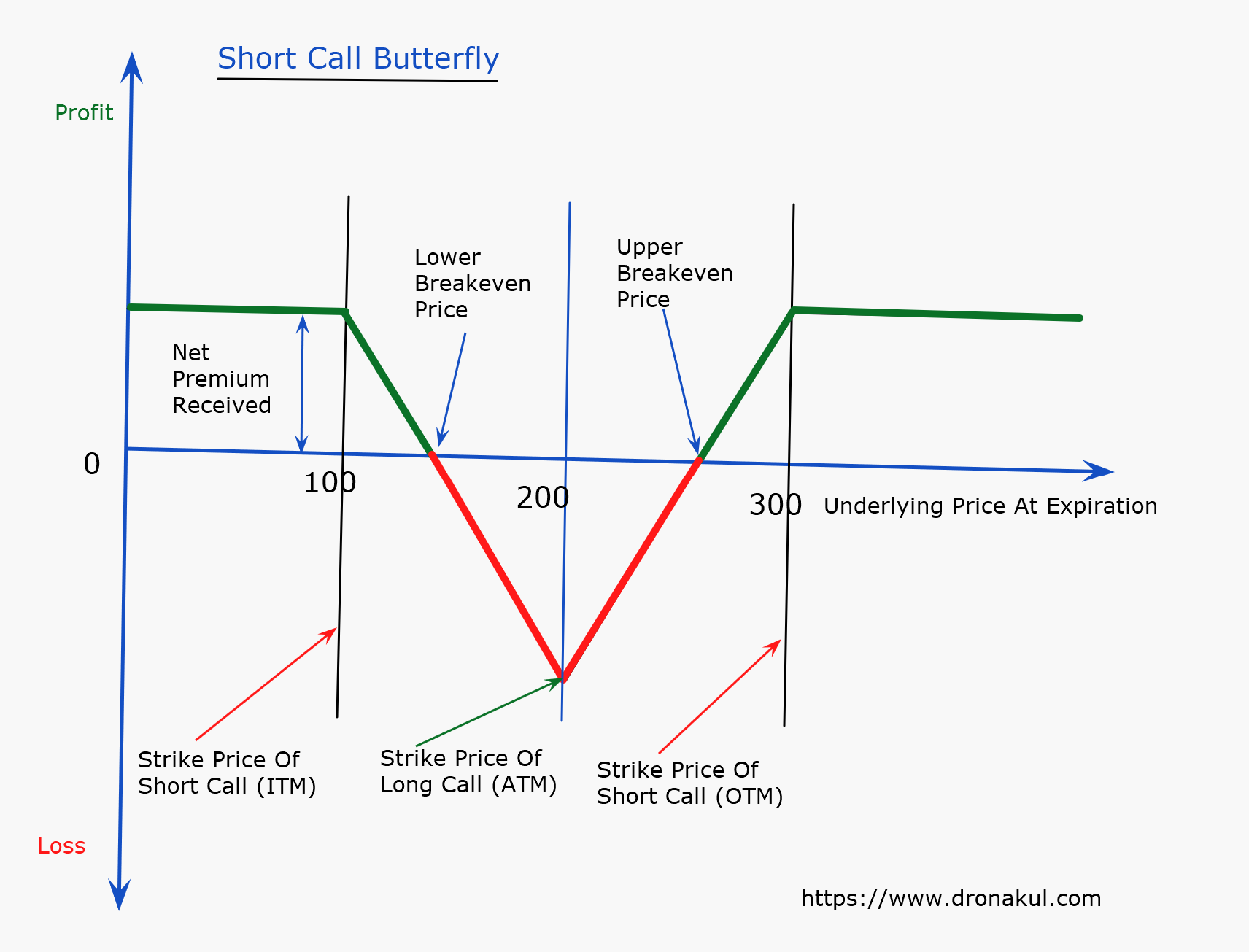

Short Call Butterfly Options Strategy

Short call butterfly is just opposit of long call butterfly strategy, it is a combination Bear Call Credit Spread and a Bull Call Debit spread, this time we receive net premium for the combined strategy.

Strategy creates when traders when the traders believe that the implied volatility will be little higher compare to long call butterfly and the underlying may close flat or lower than ATM. As credit receiveing for selling call options.

Trade Construction:

Sell 1 Lot ITM Call Options

Buy 2 Lots ATM Call Options

Sell 1 LOt OTM Call Options

Ideal Market Outlook: Implied volatility is low, Very short time remaining to expiry (1 or 2 days max), range bound market.

Profit Potential: Limited, as we receive net credit for the strategy.

Maximum Profit= Net credit received.

Maximum Loss= Strike Difference Between Traded ITM & ATM strike - Net Credit received

Upper Side Breakeven Point =Higher Strike Price - Net Premium Received

Lower Side Breakeven Point = Traded ITM Strike Price + Net Premium Received

When we can get profit?

We can get profit if the Underlying close much lower or higher than middle strike price

When we will lose money from Short Call Butterfly?

We will lose money if underlying remain flat during expiry.

Please read the below example for better understanding.

Example

See the right side picture, the Nifty Options prices are showing just after a few minutes after the market open. That time Nifty Spot price was trading around 24280.

So here,

24300CE is ATM trading at 27

24200CE is ITM trading at 88

24400CE is OTM trading at 8

I am going to show the calculation with one strike price gap.

Let us learn the strategy, its outcome and how we can create the formula steps by step

Short 1 lot Nifty 24200CE & received a premium of 88.00/-

Long 2 lots Nifty 24300CE & paid a Premium of 2*27=54.00/-

Short 1 lot Nifty 24400CE & received a premium of 8.00/-

_________________________________________________________________

Total Premium Received = 88+8=96/-

Total Premium Paid =54/-

__________________________________________________________________

Net premium Received= 96-54=42/-

First of all let's assume Nifty closed at ATM strike price

Premium of Nifty 24200CE will be 100, P/L from 24200CE =-12/-

Premium of Nifty 24300CE will be 0, P/L from 24300CE =-54/-

Premium of Nifty 24400CE wil be 0, P/L from 24400CE =8/-

----------------------------------------------------------------------------------------

Net loss will be 66-8= 58/- If we want to make up this 58 rupee loss then Nifty should close 58 points below ATM strike or close 58 point above ATM strike. As we have 2 long ATM call and 1 short ITM call, ATM call already become zero if Nifty close at ATM then no further loss form ATM, but if Nifty come down for 1 point then we will gain 1 point from Shorted ITM call options. And the moment Nifty will rise above ATM, we will earn 2 rupee from 2 lots Long ATM call and lose 1 rupee from Short ITM call until Nifty reach OTM.

So the Lower Side Breakeven=24300-58

=24242 Now see we can break 24242 as 24200+42 where 24200 is my lower strike price and 42 is net premium received. So we can write down the formula of lower side breakeven point as below..

Lower Side Breakeven Point =Traded ITM Strike + Premium Received.

In other hand we can say Upper Side Breakeven=24300+58

= 24358, Now see, we can break 24358 as 24400 -42, where 24400 is my higher strike price and 42 is net premium received. So we can write down the formula of upper side break even point as below..

Upper Side Breakeven Point= Traded OTM Strike - Premium received.

The way we have established the furmula is little bit complex specially for those who has less knowledge about arithmatics. But this steps by step process is better, in this way you can identify all the outcomes of any strategy.

Now lets understand how we can maximize the return.

Assume Nifty close at 24200 which is the lower strike price or ITM we have shorted

The Premium of Nifty 24200CE will be 0, P/L = +88/-

The Premium of Nifty 24300CE will be 0, P/L= -54

The Premium of Nifty 24400CE will be 0, P/L=+8

_________________________________________________

Net profit / Loss = 88+8-54=42

Now it is very much clear if Nifty fall below the Lower strike price (ITM Call strike price) then we will gain the maximum profit of 42 rupee.

If Nifty move up and close at higher strike price 24400, then

The Premium of Nifty 24200CE will be 200, P/L=(88-200)=-112

The Premium of Nifty 24300CE will be 100, P/L=2(100-27)=2*73=+146

The Premium of Nifty 24400CE will be 0, P/L = -8

_______________________________________________________________________

Over all profit =146-112-8

= 26/-

As this is a slidely bearish strategy, therefore we will make less profit if it rise. So we can say my maximum profit will occur when Nifty will close at or below ITM strike price (Lower strike) and maximum loss will occur when Nifty will close at ATM strike price or middle strike price. The strategy can be depolyed very near to expiry so that time value of options remain low.

Best time to deploy Short call Butterfly is when you are mildly bearish on any underlying around very near to the expiry. This strategy is not good for flat market conditions.

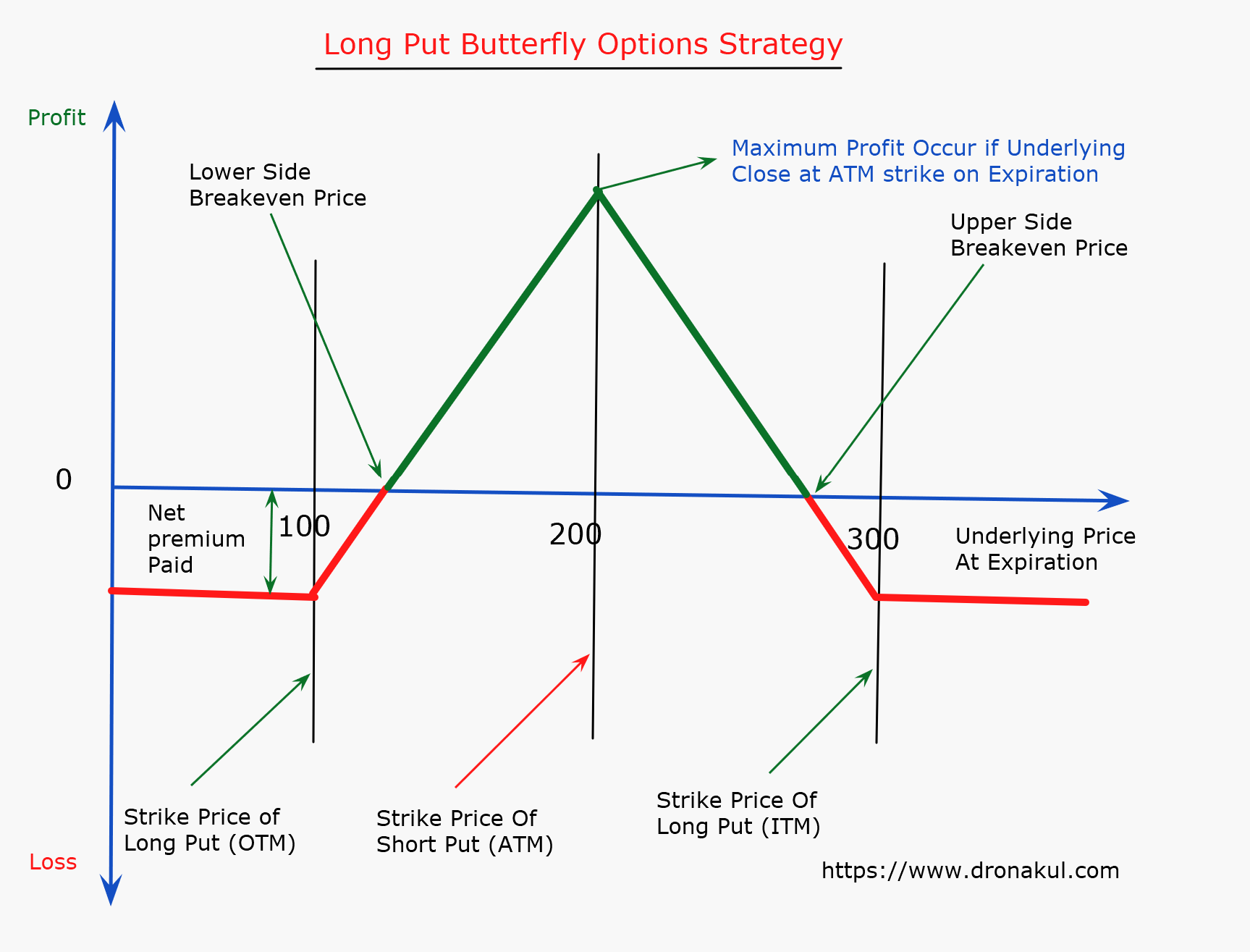

Long Put Butterfly Options Strategy

Long put butterfly is a combination of Bear Put Debit Spread and Bull Put Credit Spread, creates to make profit from low volatile or narrow range movement in the underlying assets.

Mechanics:

Buy 1 lot ITM put options

Sell 2 lots ATM put options

Buy 1 lot OTM put options

All the contact should be from same underlying and expiry.

Ideal Market Outlook For Long Put Butterfly:

When the view of the underlying price is neutral or slidely bearish, expecting the underlying will trade within a small range, traders create Long Put Butterfly to make money from time value decay.

Strategy name "Long Put Butterfly" clearly indicate that in this strategy we will pay the net premium which will be debited from our account. So we can write the formula below ..

Maximum Loss = Net premium paid

Lower Side Break Even = Lower Strike Price - Net Premium Paid

Upper Side Breakeven = Higher Strike Price - Net Premium Paid

Maximum Profit = Difference Between Traded ITM & ATM strike Price - Net Premium Paid

= (ATM Strike Price - ITM Strike Price) - Net Premium Paid

Let us check with the practical example and learn how to calculate and what will be th eprobable outcomes, we also learn the adjustment we need to do for better result.

See the right side picture for the put options prices. On 30th July 2024 Nifty spot closed at 24857.30, mean we can say Nifty 24850PE ia ATM put options.

Nifty's strike difference is 50 points. We will create the strategy without any strike price gap first and then we will create the strategy with strike price gap to understand the outcomes in different strike selection.

Long Put Butterfly Without Strike Price Gap

Long 1 lot Nifty 24900PE at 102, paid a premium =102

Short 2 lots Nifty 24850PE at 78, received a premium of 2*78=156

Long 1 lot Nifty 24800PE at 62, paid a premium of 62

_______________________________________________________________________

Total Premium Paid =102+62=164

Total Premium Received =156

________________________________________________________

Net premium paid= (164-156)

=8/-

This net premium paid is our maximum risk for the strategy, we have made this startegy as we believe that the Nifty will neamin in a range. But if Nifty moves unlimited in either side, we can't lose money more than 8/- * lot size per strategy. This low sirk startegy attract many traders to make money from low volatile market.

Imagine Nifty will close at ATM strike price 24850, lets calculate the probable outcome.

Premium of Nifty 24900PE will be 50/-, Loss =(102-50) =52 (Loss as we long it and premium reduce)

Premium of Nifty 24850PE will be 00/-, Profit=2(78-0)=156 (Profit, as we short and premium reduce)

Premium of Nifty 24800PE will be 00/-, Loss=(62-0)=62 (Loss, as we long it and premium reduce)

_________________________________________________________

Total profit =156, Total Loss=52+62=114

___________________________________________________

Net Profit=156-114

=42/-

This will be the maximum profit we can make from the strategy. Now lets test whether our formula is correct or not.

Earlier I mentioned that the formula of Maximum Profit = (ITM Strike Price - ATM Strike Price) - Net Premium Paid

= (24900-24850) - 8

= 50-8 =42

This formula is perfect.

Now Imagine Nifty close at higher strike price 24900 on expiry, let us calculate the probable outcome.

Premium of Nifty 24900PE will be 00/-, Loss=(102-0)=102/-

Premium of Nifty 24850PE will be 00/-, Profit=2(78-0)=156/-

Premium of Nifty 24800PE will be 00/-, Loss= (62-0)=62/-

________________________________________________________________

Total loss=102+62=164/-, Total profit = 156/-

________________________________________________________________

Net loss =(164-156)=8/-, If Nifty move up unlimited then also the net loss won't increase.

Nifty 24900PE is an ITM and it also become zero thats why net loss incur, if we don't want to lose this 8/- or we want neither loss nor profit then the Intrinsic Value of Nifty 24900PE should be 8/- on expiry, and it is possible if only Nifty close at 24900-8

That mean we can say our upper side breakeven point =24900 -8

Upper Side Breakeven Point = Higher Strike Price - Net premium paid

The formula I have mentioned is correct, this is how you can calculate the breakeven price, maximum profit, maximum loss etc of any options strategy. Hope the learning is going easy.

Now imagine the Nifty close at 24800

Premium of Nifty 24900PE will be 100/-, Loss=(102-100)=2/-

Premium of Nifty 24850PE will be 50/- Profit=2(78-50)=56/-

Premium of Nifty 24800PE will be 00/-, Loss=62-0=62

_______________________________________________________________

Total loss 62+2=64/-, Total loss=56/-

_______________________________________________________________

Net Loss=64-56=8/- , if Nifty fall unlimited this loss will not increase, as 2 long and short put options will give us profit loss equally.

What we found is, whether Nifty rise or fall unlimited our maximum loss will be only 8/-, which is the net premium paid actually.

So the formula of Maximum loss= Net premium paid is perfect.

Long Put Butterfly With Strike Price Gap

This time we will keep one strike gap to understand the outcomes.

But 1 lot Nifty 24950PE and premium paid 131/-

Sell 2 lots Nifty 24850PE and premium received 2*78=156/-

Buy 1 lot Nifty 24750PE and premium paid 47/-

_______________________________________________________________

Total premium paid=131+47=178/-, total premium Received 156/-

_____________________________________________________________________

Net premium paid =178-156=22/-

Upper side breakeven = Higher Strike - Premium Paid

=24950 -22

=24928

Lower Side Breakeven= Lower Strike + Net premium paid

=24750+22

=24722

Maximum Loss incur if Nifty close above upper breakeven or below lower breakeven =22/-

Maximum profit = (ITM Strike Price - ATM Strike Price) - Net premium Paid

=(24950-24850)-22

=100-22

=78/-

In first case (Long Put Butterfly without Strike Price Gap) Risk : Reward=8 : 42

=1 : 5.25

In second case(Long Put Butterfly with Strike Price Gap) Risk : Reward =22 : 78

=1 : 3.54

In my long call butterfly I explained that for more reward we should select strike price with gap between ATM and ITM and this explanation is looking little different. The reason is as currently Nifty is in strong up trend, therefore the premium of call and put options behave differently.

So during a strategy creation we must focus of market trend also.

Now the important question is which is better, selecting strike price with gap or without gap?

Both has its own positive side.

If we select strike price without gap then in aspect of Risk reward ratio it is better.

If we select strike price with gap then in aspect of ROI (Return On Investment), it is better as it has more profit potential with slightly higher margin.

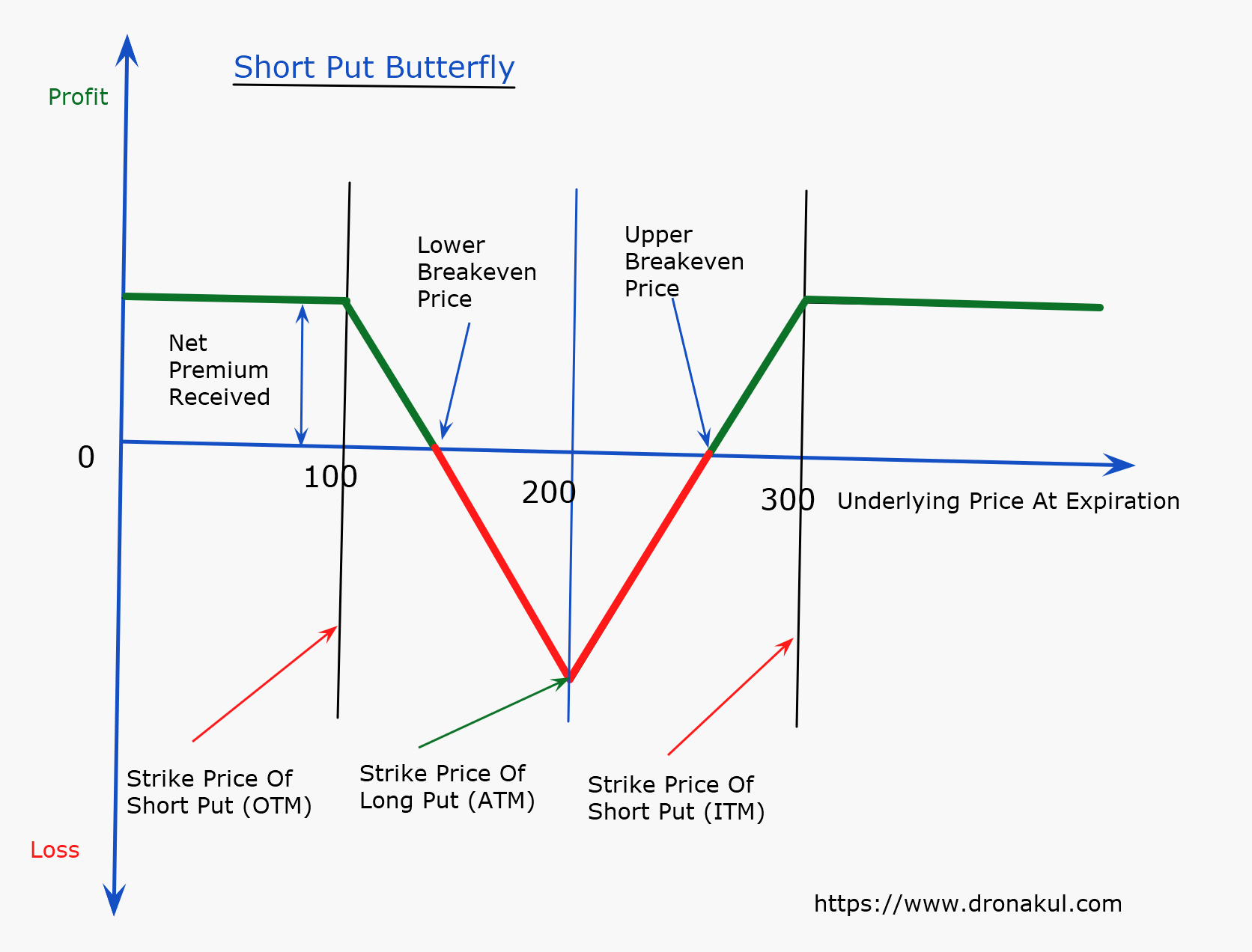

Short Put Butterfly Options Strategy

A Short Put Butterfly options strategy is just the opposite of Long Put Butterfly Options Strategy, it is a combination Bull Put Credit Spread and Bear Put Debit Spread. This time we receive net premium for the combine strategy.

When our view is underlying will be range bound but not choppy, we feel the underlying may close higher than current market price, but in a small range, we focus to make profit from short put butterfly options Strategy. It is mildly bullish strategy.

Construnction Of Short Put Butterfly Strategy:

Short 1 lot ITM Put Options

Long 2 lots ATM Put Options

Short 1 Lot OTM Put Options

This time I will not disclose the formula of maximum profit, maximum loss, and breakeven points. Instead we will learn to calculate those.

Here we will explore the strategy with the same options prices given in long put put butterfly.

Nifty closed at 24857.30 so 24850 is the ATM strike price.

Sell 1 lot Nifty 24900PE at 102/-, premium received 102/-

Buy 2 lots Nifty 24850PE at 78/-, premium paid 2*78=156

Sell 1 lot Nifty 24800PE at 62/-, premium received 62/-

Net premium received =102+62-156

= 164-156

= 8/-

As we are receiving net credit, therefore our maximum profit will be the premium we have received for the combination, here it is only 8/-

So the maximum profit = Net Premium Received

If Nifty close at higher strike price 24900, then let's calculate the outcomes.

Premium of The Nifty 24900PE will be 00, profit =102-00=102

Premium of the Nifty 24850PE will be 00, Loss = 2(78-0)=156

Premium of the Nifty 24800PE will be 00, profit=62

_______________________________________________________________

Total profit = 102+62=164/-, total loss =156/-

_____________________________________________________________

Net profit =164-156=8/-, if nifty move up unlimited, still profit wont increase more than 8/-

If nifty close 8 points below the higher strike price then the premium of the 24900PE would be 8/- and 24850PE & 24800PE would be zero and in that case neither we would make profit nor loss. So we can say ..

Upper Side Breakeven Point = 24900 - 8

Upper Side Breakeven Point = Higher Strike Price - Net Premium Received.

If Nifty will close at lower strike price

Premium of the Nifty 24900PE will be 100, profit =102-100=2/-

Premium of the Nifty 24850PE will be 50, loss=2(78-50)=56/-

Premium of the Nifty 24800PE will be 00, Profit= 62/-

__________________________________________________________________

Total profit = 2+62=64/-, where total loss = 56/-

_________________________________________________________________

Net Profit = 64-56=8/-, if Nifty fall unlimited, still profit wont exceed more than 8/-, so we can say in Short Put Butterfly Options Strategy

Maximum Profit = Premium Received

If Nifty would close 8 point above the lower strike then profit from 24900PE will be 10/-, Loss from 24850PE will be 72/- and profit from 24800PE will e 62/-, mean neither we would earn monry nor we lose. so it is the lower side breakeven point. We can write the formula like below..

Lower Side Breakeven Point = 24800 + 8

Lower Side Break Even Point= Lower Strike Price + Premium Received.

If Nifty close anywhere between Lower and higher Breakeven Point we will be in loss.

If Nifty Close at the ATM strike price, lets calculate the probable outcomes.

Premium of the Nifty 24900PE will be 50, profit =102-50=52/-

Premium of the Nifty 24850PE will be 00, loss =2(78-00)=156/-

Premium of the Nifty 24800PE will be 00, profit=62/-

_______________________________________________________________________________

Total Profit =52+62=114, total loss=156

_______________________________________________________________________________

Net loss=156-114=42/-, it will be the maximum loss as we have purchased ATM put options.

We can Say maximum loss 42=50-8

Or Maximum Loss = (ITM Strike Price - ATM Strike Price) - Premium Received

In this strategy if we select strike price with gap then premium receive will be higher, maximum losses will also increase marginally, but profit potential will increase dramatically.

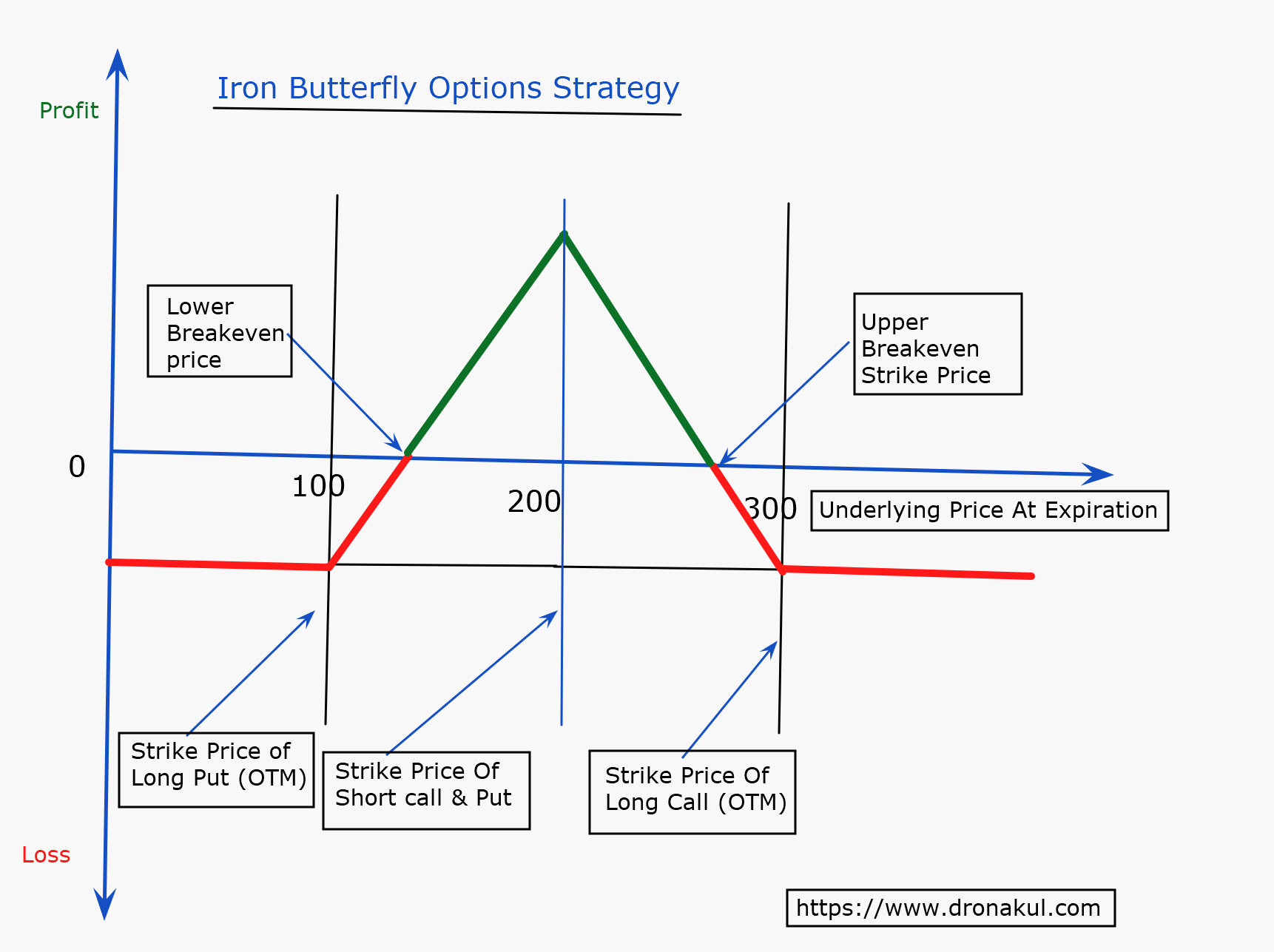

Iron Butterfly Options Strategy

Iron Butterfly is a combination of two credit spread, one bear call spread or Call Credit Spread another bull put spread or Put Credit Spread, created when the traders believe that the underlying may close in very tight range, expected closing is near to ATM strike price. It is a neutral strategy.

Timing Risk: This strategy involves timing risk, the more time remaining to expiry the more risky.

Strategy Construction:

Sell 1 lot ATM call Options

Buy 1 lot OTM call Options

Sell 1 lot ATM Put Options

Buy 1 lot OTM Put Options

As this is is a completely educational purpose, I will explain it steps by steps, so that you can understand the risk, reward, management, adjustment and can come to know the entire outcomes of the strategy. I will teach you how to identify the maximum profit, maximum loss, breakeven points etc. let's drive deep into the calculation. I am going to give you practical example based on Nifty options closed on 31st July 2024.

See the right side picture of Nifty options, these are the last traded price on 31st July 2024. Nifty spot closed at 24951.15, so 24950 is the ATM strike price. See the strategy construction below

Sell 1 lot Nifty 24950CE at 99, premium received 99

Buy 1 lot Nifty 25000CE at 73, premium piad 73

Sell 1 lot Nifty 24950PE at 68, premium received 68

Buy 1 lot Nifty 24900PE at 50, premium paid 50

Net premium received for Bear Call Spread = (99-73)=26/- & Net premium received for Bull Call Spread = (68-50) =18/-

Total Net Premium Received=26+18=44/-

As Iron Butterfly is a cambination of cann and put credit spread, therefore our maximum profit can not exceed more than the Total Premium Received. So we can say in Iron Butterfly, Maximum profit = Total Premium Received

Now let us understand when it is possible, we have three different strike price number and those are 24950, 25000 and 24900, now we will calculate three different scenario assuming the Nifty will expire on those strike prices to understand the whole strategy in depth. First of all,

lets assume Nifty will expire at ATM strike price 24950, then we will gain the maximum profit as I have discussed in earlier study of Bear Call Spread and Bull Put Spread that if the Underlying close at Sold Strike Price on expiry then we will receive the maximum profit. Here again showing you the calculation.

Premium of the Nifty 24950CE will be 00, profit =99/-

Premium of the Nifty 25000CE will be 00, loss=73/-

Premium of the Nifty 24950PE will be 00, profit=68/-

Premium of the Nifty 24900PE will be 00, loss=50/-

_____________________________________________________________________

Total profit =99+68=167/- and Total loss=123/-

_____________________________________________________________________

Net Profit =167-123=44/-

If Nifty Close at 25000, then

Premium of the Nifty 24950CE will be 50, profit = 99-50=49/-

Premium of the Nifty 25000Ce will be 00, Loss=73-0=73/-

__________________________________________________________________

There will be loss for the Credit Call Spread of 73-49=24/-, where ...

Premium of the Nifty 24950PE will be 00, Profit=68-0=68/-

Premium of the Nifty 24900PE will be 00, Loss=50-0=50/-

__________________________________________________________________

There will be a profit for the Credit Put Spread of 68-50=18/-

Overall situation is there will be a loss of 24-18=6/-, after 25000, if Nifty rises unlimited then there will be no difference of losses, as the sold call option will give us loss, where bought call option will give us equvalent profit for the up move. So our maximum loss in this strategy will be only 6/-.

Now question is how to formulate it?

We can say 6=50-44, 6=Maximum loss, 50=Strike difference between traded ATM and OTM, and 44= Net premium Received

So the formula of Maximum Loss=Strike difference between traded ATM and OTM - Net Premium Received.

Notice that we are goig to lose 6/- if the Nifty Move up, so what will be our upper side breakeven point? The process of thinking is very easy, find which strike price call options actually giving us profit, here 24950CE has given us profit for selling and the amount is 49/-, if we able to earn 6/- more from the same call then neither we were in profit nor in loss. So Nifty should close 6 points below The higher Strike Price.

We can say the formula of Upper Side Breakeven Point=Higher Strike Price - (Strike Difference Between ATM & OTM - Premium Received

Now let us understand the outcomes if the Nifty close at 24900

Premium of The Nifty 24950CE will be 00, Profit =99/-

Premium of the Nifty 25000CE will be 00, Loss=73/-

________________________________________________________

For this Credit Call Spread Profit=99-73=26/-, where

Premium of the Nifty 24950PE will be 50, profit=68-50=18/-

Premium of the Nifty 24900PE will be 00, Loss=50/-

________________________________________________________________

For this Credit Put Spread loss=50-18=32/-

____________________________________________________________________

Overall losses for the combination =32-26=6/-, same outcome, that mean now we can say, na matter underlying moving up or down, the Maximum Loss is fixed either side for unlimited movement.

Now if we try to understand about, what will be our lower side breakeven point then first we shall find out which put options has given us profit, we have to earn the maximum loss amount more from that put options. Here 24950PE has given us profit of 26/- for selling, so we can say if Nifty would close 6 points above the lower strike price, then we would make 6 rupee more from 24950PE, remaining all other options would have no change.

So we can say,

Lower Side Breakeven Point = Lower Strike Price + (Strike Difference Between ATM & OTM - Net Premium Received)

Risk Reward and Timing:

If we select strike price without gap then normally this strategy represent low risk, high reward probability, but as it offer maximum profit while spot price expire at ATM, therefore the accuracy of making money from this strategy is very less. Anyone will be attracted by it's Risk Reward offering but the fact is hardly 4/5 times only the strategy is suitable even for the professional.

Normally we noticed when market or underlying is awaiting for a big event, then the movement of the underlying prices remain very flat. So if any Expiry Date fall before the event then professionals deployed Long Call Butterfly, Long Put Butterfly or Iron Butterfly. So before you deploy any butterfly strategy watch the options behaviour, tak a note of them, create data base and do practice with paper trading.

Holding period For Butterfly, Challanges For Volatility:

In my all examples I have shown you that most of the butterfly represent low risk high reward trading opportunity, but butterfly strategy requires less volatile market, this is where you can face tough challange, sometimes you can see sudden volatility increase in underlying. Maximum traders fail into delema whether they should carry the butterfly position till the expiry or exit with a loss (When implied volatility increases losses incur for the strategy), early exits always offer more than predetermind risk.

It means if you exit early due to volatility, will lose more money than you have claculated maximum loss for the strategy, even if you try to adjust with other options leg chances of making mistakes will increase and loss may increase dramatically.

When you are deploying a butterfly strategy, you are ready to afford the calculated maximum loss then only you are creating the strategy na? So why afraid due to volatility? Your loss can't exceed more than your calculated maximum loss as discussed in different strategy. My suggestion is very simple, stay sticky with your position when volatility increased during a butterfly, as already you are agree to afford the calculated risk.

Learn About Options Terminology & other Options Strategies

Feel free to send your feedback or suggestion realated to butterfly strategies, also let me know if there in any part where more improvement needed. Thank you.