Study Options With Dronakul's Options Trading Course: Your Guide to Mastering the Options Market

Welcome to Dronakul's easy-to-follow options trading course! Whether you're an experienced investor wanting to learn more or a beginner curious about options, this course will give you the skills and knowledge you need to succeed.

I'm here to make options trading simple and clear, giving you a strong understanding of the basics to advance of options trading. From learning key concepts to discovering advanced strategies, we cover everything. I believe that understanding is powerful, and our course helps you make smart choices in the ever-changing world of options trading.

This options trading course has course content is extremely rich with beginner's friendly explanation.

What You Will Learn In This Options Trading Course?

We will cover both part, Options Terminology and various Options Strategies

Options Terminology

Options Strategies

What Are Options?

An Options is standardized financial contract, with a certain limited life, gives the buyers the right, but not the obligation to buy or sell an underlying asset at a specific price, on or before a certain date.

It has two contracting parties, one buyer and another seller (Also known as options writers).

It is a regulated security, just like a stock or bond, and constitute a binding contract with strictly defined terms and properties.

Options buyers get the right of Exercise and pays a price called Premium , where options sellers assume the obligation of assignment, in exchange of receiving the payment (Premium).

That mean, options buyers can only lose the premium they have paid for the right, options writer will gain maximum the premium they have received. If the underlying price gives a significant movement towards buyers direction, the options premium will increase undefined, so we can say maximum profit for the options buyers could be unlimited where loss for the options writers could be unlimited.

In a single sentance, for options buyers, risk is limited and reward is unlimited; where, for options sellers (options writers), reward is limited and risk is unlimited no matter Call or Put.

Why Options Trading Is Complecated?

Options trading are very tricky, it is very dificult to know when and how to use options and how to predict their worth. Complete and in-depth knowledge on technical analysis, options terminology, and how the options behave are important for options trading. For successful options trading, proper combination of excellent technical analysis knowledge, options terminology, options data and descipline are required.

Real traders make money from options because they know how to make assesment of the probability of the direction of the trade and they are able to identify unusal characteristics of an options. Before the entry, they identify a directional move in the underlying asset and any change in volatility.

Many traders lose money because of bad timing in directional options trades, and bad timing of the volatility of the options trade.

Timing of trading in options is utmost important part, so depth knowledge of Technical Analysis is the main key of options trading.

Why Trade Options?

People trade options for many reason,

- Leverage: Leverage mean you are paying a small amount of premium and controlling a large amount of underlying asset, options contract represent multiple number of shares of an underlying. It sold in a lot. So when you buy an options, you are paying a small amount as a premium which is just a fraction of the total value of the lot size, but it allows you potential profit from the underlying movement without investing a large amount of money upfront.

- Portfolio Protection: Another popular use of options is to protect your portfolio against downside risk of your capital due to any known or unforeseen events. You can use options to give a potection both to your long or short trade. If you have long position and you are afraid the market can go down you can hedge your long position buying put options against it, or if you have sold something and afraid that underlying or future contract may move up then you can hedge your short position buying call options.

- Built In Stop Loss: If you are a buyer of an options then you are controlling a large amount after paying a small premium, and if the trade goes against you, then you will lose only the Options Premium you have paid, but if you hold the large quantity of underlying itself you would lose lots of money. So as a buyer you have an inbuilt stop loss. You can't lose money more than the premium you have paid.

- Customized Various Strategies: People use options to create wealth from customized various strategies from any movement of the underlying with minimum risk.

Call Options

Call options gives buyers the right but not the obligation to buy the underlying at a specific price on or before a certain date. people purchase a call options when they have bullish view on the underlying asset and sell (write) call options when they have moderately bearish view on the underlying asset.

The premium of a call option is directly proportional to the underlying price, meaning if the stock price rises, the premium of the call option will rise, and if the stock price falls, the premium of the call option will fall.

Call option buyers pay the premium, while sellers receive the premium.

Risk & Reward: Call option buyers have unlimited reward potential and limited risk. If the stock price rises quickly, the premium of the call option may increase to an undefined price. However, if the stock price falls or remains stable, the premium of the call option will become zero, so buyers can only lose the premium they paid if their view is incorrect. On the other hand, call option sellers face unlimited risk and limited reward. If the stock price rises significantly, the option premium will also rise significantly, and the seller could lose a large amount of money. However, if the stock remains choppy or declines, the premium will become zero, and the seller will keep only the premium they received from selling the call option.

Let me explain the definition in simple manner.

Assume PQR Ltd trading at 500 and you are bullish on it, and you have purchased 510CE and paid a premium of 12/-. Lot size 1200.

On expiry day you saw the stock is trading at 550 and your 510CE trading around 40/-, you are in profit now. You can sell the contract to book profit. But if you thing the underlying has much more upside potential in near future then you can exercise the options, mean you can convert your options lot into 1200 quantity (As lot size mentioned 1200) of Equity. In this case you have to pay an amount of 1200*510 to the exchange, and then you will receive delivery of PQR Ltd in your demat. See here you are paying at 510, this was your strike price.

Now imagine The stock has come down to 480 on the expiry, the the premium of the options will become zero. Now you can let the options expire and do nothing. But if you wish to exercise, you can. In that case you have to inform the exchange and pay the same amount like earlier 1200*510, and you will receive delivery of PQR Ltd. Obviously exercising an out-of-the-money (OTM) call options is a foolish decision, but as you have the right to buy but not obligation, therefore you can exercise if you wish only when the options is OTM

Now assume you are a seller of 510CE of that PQR Ltd and receive the premium of 12/-, on expiry the stock is trading 550, so call options premium will be 40/- . Now you must book loss here and buy back he contract, if you fail to do so then you have the obligation to give a pay out of 1200 quantity of PQR Ltd to the exchange. Else a huge penalty you have to pay.

In other case, assume the stock of PQR Ltd expire at 480, so you are going to keep the premium with you. But if any buyers of that 510CE wish to exercise the options contract at a loss then exchange will do a random lottery with those who sold 510CE but did not close the position from their end, whom they will catch in lottery, he / she has to give a payout of 1200 quantity of PQR Ltd. Normally it won't happen, as people do not exercise when a call options expire as OTM, but as per the rule it is possible.

Put Options

Put Options

Put options give buyers the right, but not the obligation, to sell the underlying asset at a specific price on or before a certain date. People purchase put options when they have a bearish view on the underlying asset and sell (write) put options when they have a moderately bullish view on the underlying asset.

Premium of a put options is inversly proportionate with the underlying price, mean if the stock price rise, then premium of a put options will fall, and if the stock price fall, then premium of the put options will rise.

Put options buyers Pays premium where sellers receive premium.

Risk: Put options buyers reward is unlimited where risk is limited. If the stock fall faster the premium of the options may rise upto a undefined price. But if the stock rise unlimited or remain stand-still then the premium of the put options will become zero, so the buyers can lose only the premium they have paid if their view is not correct. But put sellers risk is unlimited and reward is limited. If the stock fall unlimited then the options premium will also rise unlimited and the seller will lose huge amount of money, but if the stock become choppy or move up faster then the premium will become zero and the seller will keep only the premium they have received during selling the put options.

Let me explain the definition in a simple manner.

Assume PQR Ltd is trading at ₹500, and you are bearish on it, so you purchase a 490PE and pay a premium of ₹12. The lot size is 1200.

On the expiry day, you see the stock trading at ₹450, and your 490PE is trading around ₹40. You are in profit now. You can sell the contract to book the profit. But if you think the underlying has more downside potential in the near future, you can exercise the option, which means you can sell 1200 shares (as the lot size is 1200) of PQR Ltd if you have it in your demat. In this case, you will receive an amount of 1200 x 490 from the exchange. See here, you are receiving payment at ₹490/share from the exchange, which was your strike price.

Now imagine the stock has risen to ₹520 on expiry; the premium of the option will become zero. You can let the option expire and do nothing. But if you wish to exercise, you can. In that case, you have to inform the exchange and deliver the shares at the same price as earlier, 1200 x 490, to the exchange. Obviously, exercising an out-of-the-money (OTM) put option is a foolish decision, but as you have the right to sell, not the obligation, you can exercise if you wish, even when the option is OTM.

Now assume you are the seller of a 490PE of PQR Ltd and receive the premium of ₹12. On expiry, the stock is trading at ₹450, so the put option's premium will be ₹40. You must book a loss here and buy back the contract. If you fail to do so, you have the obligation to buy 1200 shares of PQR Ltd at your strike price 490. Otherwise, you have to pay a huge penalty.

In another case, assume the stock expires at ₹520, so you keep the premium with you. But if any buyers of that 490PE wish to exercise the options contract at a loss, the exchange will do a random lottery with those who sold 490PE but did not close their positions. Whomever they select in the lottery has to buy 1200 shares of PQR Ltd. Normally, it won't happen, as people do not exercise when a put option expires as OTM, but it is possible as per the rules.

Normally, in Index options rights and obligations are not applicable, for index options cash settlement done from the exchange end with a small penalty in case long options expires as in-the-money options (ITM).

At-The-Money (ATM) Options

At expiry when Strike Price and current market price are equal, called At-The-Money options. Before expiry, if you select a strike price which is nearest to the current market price of the underlying, is called At-The-Money options.

For example, assume PQR Ltd trading at 542.6, a few days remaining to expire, strike difference is 10, now if you buy 540CE or 540PE, will be consider as ATM call or put options respectively. But on the expiry if stock close at 540 then only 540CE & 540PE will be consider as ATM call or put options.

At-The-Money Options => Current Market Price = Strike Price

In-The-Money (ITM) Options

An options is said to be "In-The-Money" if any money could be brought in by exercising the options and liquidating the position.

Perhaps the definition is little complex. Let me explain it in simple manner.

In Buyers aspect, if we buy an options it means we receive a right to buy or sell an underlying at a specific price, so we can say if we buy a call options we are assuming (Not in real) that we have purchased the underlying at the strike price. Assume we have purchased a 540CE of PQR Ltd, it means We are thinking that while PQR Ltd was trading at 540, we have purchased PQR Ltd. Now if PQR Ltd trade above 540 then we can say that our trade running in profit. Now here, 540CE will become In-The-Money call options because our assumption is running into a profit.

So in case Call Option, we can say

In-The-Money Call options=> Current Market Price > Strike Price

So we can say if PQR Ltd trading at 540 then every strike price below 540 are ITM Call Options

Oppositely we can say if we buy 540PE of PQR Ltd then we are assuming (Not in real) that while PQR Ltd was trading at 540, we have sold out PQR Ltd, if PQR Ltd strat trading below 540 we will be in profit. Now we will say this 540PE has become In-The-Money put options.

So in case Put Options, we can say

In-The-Money Put options=>Current Market Price < Strike Price

So we can say if PQR Ltd trading at 540 then every strike price above 540 are ITM Put options

Only in-the-money options have Intrinsic Value

Out-Of-The-Money (OTM) Options

An options is said to be Out-Of-The-Money, if there is no economical benefits for excercise the options as a mean of liquidating the position. In other word if you exercise the position you would actually have a negative balance.

Let me explain this in very simple manner.

Assume, PQR Ltd is trading at 540 and we have purchased a call options of 560 strike, it means we are assuming that while PQR Ltd was trading at 560, we have purchased PQR Ltd, now see CMP is 540 mean we are running into loss. Now if we inform the exchange that we will exercise the position mean we will pay at a rate of 560/share and take delivery then it is actually a blunder, where we can buy PQR Ltd at 540 from the open market. Here 560CE is OTM when CMP is less than 560.

So In case of call options we can Say,

Out-Of-The-Money Call options => Current Market Price < Strike price

So we can say if PQR Ltd trading at 540, then every Call options strike prices above 540 are OTM call options

Oppositely, we can say if PQR Ltd trading at 540 and we buy 520PE it means we are thinking that while ABC Ltd was trading at 520 we have sold out PQR Ltd, that mean currently we are running into loss, money going out from out pocket. If we inform the exchange that we want to give delivery of the PQR Ltd at 520, we will lose money. This is what we call no benefit for exercising the options position.

So we can say, in case put options

Out-Of-The-Money Put Options =>Current Market Price < Strike Price

So we can say, if PQR Ltd trading at 540 then, every put options strike price below 540 are OTM Put Options

An out-of-the-money options Premium consists only Time Value

Compare Between Stocks and Options

Stocks

- Actively Traded in a listed market.

- Buyers make bids, seller makes offer.

- Have a shares of a company, have get voting rights, receive dividend.

- Has no expiry date.

Options

- Actively traded in a listed market.

- Buyers make bids sellers make offers.

- Derivatives, derives from an underlying securities.

- Numbers of contract available for the same underlying.

- Have expiration dates.

Strike Price

In a simple language, strike prices are the Exchange Prices of The Asset, it is a predeterming price, at which the buyers of an options contract can buy (in case of call options) or sell (in case of put options) of the underlying asset.

For example, assume you have purchased a Call options of PQR Ltd, strike price 540. It means if you exercise PQR Ltd on expiry then you will receive the stock in your demat account at a rate 540/- per share. That time no matter where the stock is trading.

Oppositely if we purchase 540PE of that PQR Ltd and we exercise on expiry then we have to give a pay out of PQR Ltd to the exchange, equal quantity of options lot size, in exchange we will receive a payment of 540/- per share from the exchange.

Strike Price selection in options trading is one of the most important part.

Options Premium

Options premium is the price which buyers pay to the options sellers to receive their right. Options premium consists two value, one is Intrinsic Value another is Time Value. Options Premium depends on several factors.

Like Intrinsic Value, Time Value, Implied Volatility, Interest Rate and Dividend.

Intrinsic Value

Intrinsic value is simply the difference between current market price of the stock and strike price, only ITM options have intrinsic Value. Negative intrinsic value is consider as zero. On expiry, options premium is equals to intrinsic value.

Remember, on expiry day, options pricing totally depends on its intrinsic value. On expiry if an options has no intrinsic value then the options will expire worthless. This is why, options buyers looks for more intrinsic value in an options.

In more simple language we can say, "If we would really Buy or Sell the Underlying at it's strike price, then the profit would occur as per current market price, are called intrinsic value."

For example, assume PQR Ltd is trading at 500, and you have purchased 490CE.

In simple language I can say, if I buy 490CE of PQR Ltd, it means to me that, I am assuming I have purchased PQR Ltd at 490, this is just my right to buy, but if would buy it originally then what would happen? I would be in a profit of 10/-

My assumption, my purchased price is 490, and current market price is 500, so I would be in a profit of 10/-

We can say...

Intrinsic Value Of A Call Options = Current Market Price of the Underlying - Strike Price

In other hand, lets assume I have purchased 510PE while PQR Ltd was trading at 500, buying a put options mean right to sell, in simple language, I am assuming that I have sold PQR Ltd at the rate of 510 and currently PQR Ltd is trading at 500, so my assumption is running into a profit of 10/-. So this is the intrinsic value of 510PE

We can say...

Intrinsic Value Of A Put Options = Strike Price - Current Market Price Of The Underlying.

Remember, Intrinsic Value is only affected by the change of underlying price, it never waste away or decay.

Time Value & Time Value Decay

When we buy or sell an options we pay or receive premium respectively, this options premium is a sum of Intrinsic Value and Time Value, this time vale is the additional amount of money over and above the Intrinsic value in an options premium.

All OTM & ATM options are consists only time value.

We pay time value during buying an options for the Time remaining to expiry, in other word we can say we buy time to expiry of an options and pay an amount called time value.

Time Value = Options Premium - Intrinsic Value

As we are buying time using time value, it gradually decreases as well as time to expiry decreases. This is what we call Time Value Decay. In other word we can say options sellers sell time to expiry and receive time value, as well as time to expiry decreases, probability increases for the options sellers that they could make profit if the underlying has very less movement.

Understanding the movement of the underlying using time value: Time value represent a consencious opinion about the underlying trend very often, and a trader can guess the direction of the underlying. For example, assume the stock of PQR Ltd is in up trend, now we need to check the ATM call and PUT options when a buying scenario will occure. Assume it has approached a Demand zone, we need to check what is the value of ATM call and put both? Normally the premium of both call and put options of the same underlying and expiry should have almost equal premium, but traders feel price will respect the demand faster then the premium of the Call options will be much more higher than put options premium. This is happen because selling a call options is more risky than selling a put options when price about to rise. So sellers of the options looks for more time value to take the risk of selling.

Opposite is also true, if the trend is down and price approached a supply zone, we need to check the premium of ATM call and Put options both, if the premium of the put options is much more higher than the call options premium, it indicates that professionals view on this underlying is bearish, most probably price will respect the supply zone and fall, that's why sellers of the put options, are looking for more time value as it is more risky to sell.

Time Value Decay: If you buy an options and your view is little bit incorrect, mean neither the underlying moving in the direction of your trade nor it is against your view, then the options premium gradually decreases as time value decreases due to time loss, however, you can attribute the remaining time value before expiry by selling the options, but at expiry no value will be attributable.

Normally ATM options have more time value than ITM and OTM options.

We see less time value decay in ATM options during early in the expiry where ITM & OTM options time value decay are liner, and we see as well as expiry approaches, time value decay occur faster.

In an options premium we see more time value during early in the options contract expiry as the more probability is there that, the options may become In-The-Money if more time remaining to expiry.

Time value depends on many things as follow:

Time To Expiration: The more time remaining to expiry, the more time value available in an options premium.

Interest Rate: The cost of money to holding the underlying affect on time value, more interest rate mean more time value.

Stock Price: If the stock price is far away from the options it implies that, there are less probability that the options will move to ITM till the expiry. This is why OTM options cheaper than ATM or ITM.

Strike Price: Stock Price entry if the options is exercised.

Call or Put: Due to exercise availability of options, call and put of the same underlying and expiry can have different amount of time value.

Implied Volatility

Implied Volatility totally depends on options prices, it is a measure of the market's view or prediction the future volatility of an option.

It represents the crowd psychology and can move to unreasonable extremes. The extreme move can be instantaneous.

This extreme instantaneous move can kills options sellers winning probability. A sudden rise in implied voaltility is the key enemy of options writes. Where rise of implied volatility is a good friend of options buyers. But this is not truth always.

During an event, implied volatility remain higher, and it discounted in options premium far before the event declare. Once the event declare, the implied vlatility fall faster than expectation and a buyers of the options may lose maoney faster than they expected.

For example, assume after 5 days, there is a big event like some election result to be declare or union budget to be declare in the parlament. Today you will see the premium of every options are too high, at least double than the normal days. Because market expecting a significant movement either side after the event, but from the begening of the expiry it has discounted the implied volatility before the event happen. Now assume, Nifty is trading at 24000, we see expiry remaining 7 days (lets assume it is weekly expiry), now you will notice this thing that if the premium of an ATM call or put options of Nifty is around 200/- at the beginning of the expiry, then this time the premium of Nifty's ATM call or Put options will be somewhere around 400/-

That mean If we buy any ATM call or put options of Nifty, our breakeven point will be 400 points away than current market price. So our chances will be very low to make good profit, not only that but also we can say, if, by chance market goes against our direction we will lose lots of money.

Therefore we can say, if the implied volatility already discounted in the options price, never it is a good idea to buy the options, instead when the event is over and if we have knowledge what should be the impact in the market of that event, we can sell options of opposite direction. If the probable outcome of the event is market will move up then selling put is better than buying a call as call options premium may fall due to Implied volatility decrease after the event. And vise versa.

In other hand we can say, if Implied Volatility increases due to some unforeseen event then it will kill the options sellers trade. It has been noticed that during the expiry day, when no declared event is available, Implied volatility increases suddenly and kills options seller trade. So options writers must watch their position on expiry date and should trade with strict stop loss.

Breakeven Price

If we hold an options position till the expiry then at a certain price of the underlying, neither our position remain in profit nor in loss, that certain price of the underlying is called Breakeven Price.

Let us learn to calculate the Breakeven Prices for both call and put options.

Assume we have purchased 500CE of PQR Ltd and paid a premium of ₹22.00, we carried it till the expiry. Earlier we have already learnt that on expiry, only the Intrinsic Value remain in the options premium. That mean if we able to sell our call options at ₹22.00 then neither we will be in loss nor we will be in profit.

We know that, Intrinsic value Of a Call Option = Current Market Price - Strike Price, let's assume PQR Ltd expire at X which is current market price or Breakeven Price

22= X - 500

X=500+22

Breakeven Price= Strike Price + Premium

If we sell the same options then we have to buy back the option at expiry at ₹22.00 then neither we will gain profit nor we lose money. That mean again ₹22.00 is the Intrinsic Value of the options. We have to buy at intrinsic value only. like earlier we can calculate ..

Intrinsic value = Current Market Price - Strike Price, if the CMP or breakeven price is X then

22= X - 500

X=500+22

Breakeven Pricet Of a Call Options= Strike Price + Premium

So, We can Say, no matter whether we buy or sell call options,

The formula of Breakeven Price of a Call Options = Strike Price + premium

In similar way we can calculate the breakeven price for a put options, no matter we are buyers or sellers..

Breakeven Price Of A Put Option=Strike Price - Premium

India Vix

The India Vix a measure of implied volatility for the Nifty. It can be charted and the range could be zero to well over 60, though reading above 40 are very rare. After the implementation of India Vix only once it reached more than 80 during the market crush in fear of pandemic in Feb-March 2020.

India Vix is inversly proportionate with Nifty, if Nifty moves up strongly, India Vix decline, and if The Nifty fall sharply, the India Vix rises dramatically.

It is also called fear index for Nifty. When traders expect higher volatility the demand of Out-Of-The-Money options increases and the Invia Vix also increase. Oppositely, when traders don't expect higher volatility, the demand of OTM options decrease dramatically and reading of India Vix also.

India Vix is lagging indicator, not useful for short range, it just help traders to understand whether market will be volatile or not.

Sometimes India Vix can signal us about the turning point of the broader market with the demand supply context. If Nifty fall sharp India Vix rise dramatically, if Nifty fall at or near the extreme demand zone and India vix reading greater than 25 the panic has reached a frenzy, the combination indicates that Nifty probably around the bottom. Opposite is also true, when Nifty rises in a bullish trend, the volatility index drops gradually, in the mean time in India Vix reading is lower than 11 and then within a month Nifty creates two more selling scenario, it indicats about a short term top in Nifty.

In other word, we can say India Vix helps trader to prepare for a reversal trading after a significant up or down trend, in short term trading it only let the trader understand whether they should be a options buyers or sellers.

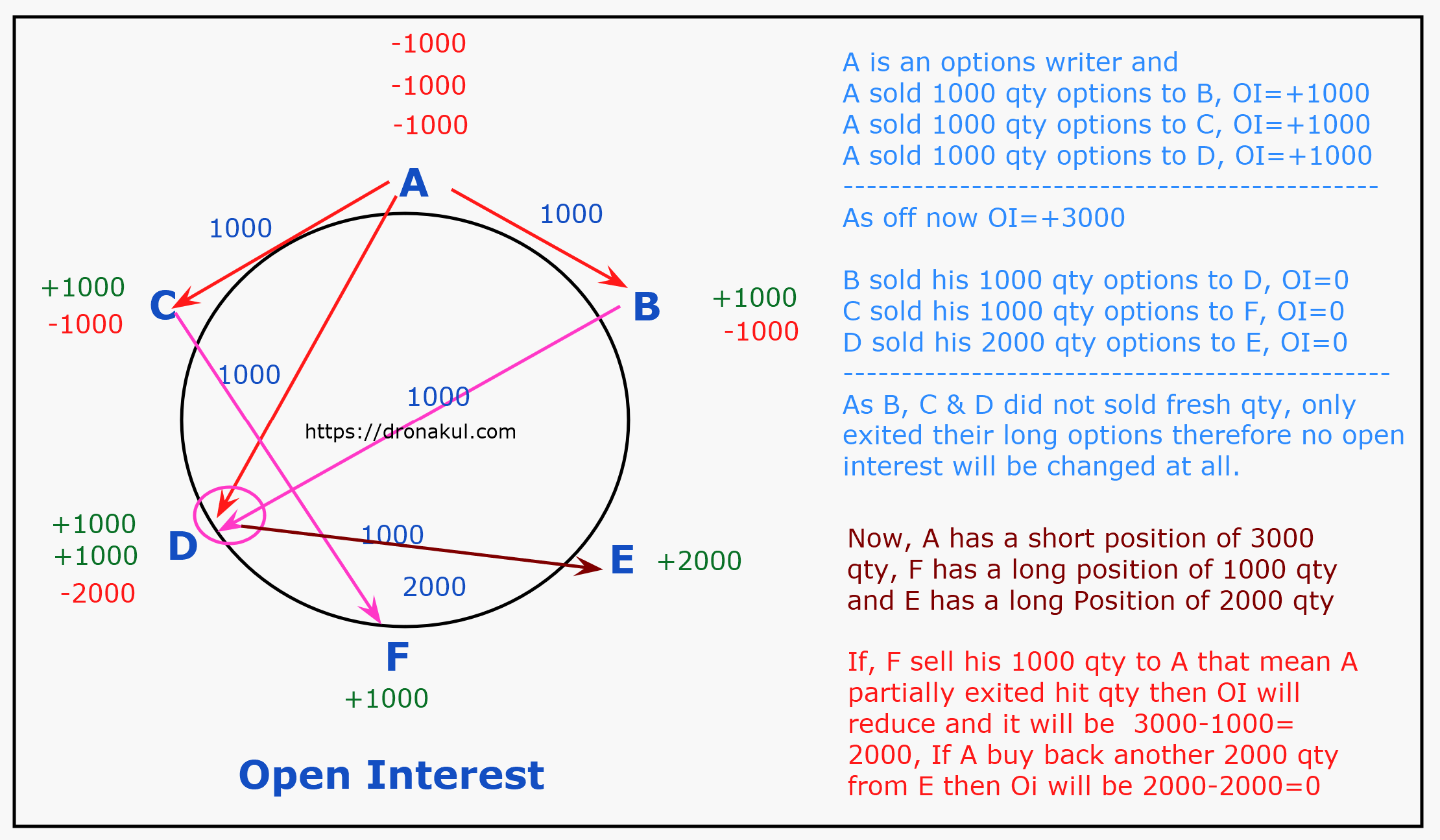

Open Interest (OI)

Open Interst is the total number of outstanding options contract of a specific underlying, strike price and expiry, which are neither exercised, nor expire or even offset the position, instead, currently active in the market.

To understand better, see the right side diagramm carefully.

Assume A sold 1000 quantity each, 500 strike price call options of a PQR Ltd to B,C & D. The total OI =3000

Now asssume B sold his 1000 qty to D at a profit or loss, C sold his 1000 qty to F at a profit or loss, D has sold his 2000 qty to E at a profit or loss, there will be no change in OI as they are offestting the position only. If A buy back all 3000 outstanding qty then OI will be zero.

Open interest is different than volume, for the above case A sold total 3000 qty and OI=3000, volume =3000,

When B sold his 1000 qty to D, volume will be increased another 1000 qty but in open interest, there will be no change.

Increase in call options OI mean people are selling more call options, we call it open interest build up in call options, So Open Interest build up in call options refferes bearish view on that underlying.

When open interest decrease in call options it means, seller of the call options are setting off their sold call options or exit form the sold call, we call it Unwinding Of Open Interest in call options, this reffers the end of bearish view.

When open interest increase in put options, it means, traders are selling more put options, we call it Open Interest Build Up in put options, this reffers bullish view on that underlying.

When Open Interest Unwinding of a put options reffers the end of a bullish view.

Normally Call Options OI Build Up is higher when price reach to a technical supply zone or creates any selling opportunity, and unwinding occurs when price reach near to a demand zone.

Similarly, Put Options OI build Up occurs when underlying price reach to a demand zone and unwinding occur when reach to a supply zone.

Why Open Interest Is Important?

Open Interest data give us clear vision about underlying direction as well as options pricing. If OI of a call options build up faster, it implies a sharp downfall in the underlying and oppositely Faster OI buid up in Put options implies a significant up move in the underlying. We need to check how fast the OI changing. Higher open interest also implies more liquidity in options market.

Use of Open Interest

Uses of OI data is very complecated, a deeper understanding of demand supply and technical analysis is essential. Increase of far OTM options open interest normally reffers a range bound market, OI build up in ATM options reffers a short term reversal of the price, where OI build up in Deep ITM reffers a long term strong reversal in price. Build up of open interest with volume represent strong reversal going to take place.

Can Open Interest Data Mislead Traders?

Sometimes, OI data mislead options traders. We all know that OI build up in call options mean traders showing bearish view on the underlying, sometimes professionals can sell call options as a hedge of their equity or future long position. But this will show in OI data and can mislead options trader. For example, assume you have purchased a stock PQR Ltd at ₹500, as per technical your stop loss is 490 and target till the expiry 530, you are moderately bullish on it. You saw the 500CE trading at ₹23.00, lot size is 2000, so if you buy 2000 quantity of PQR Ltd you have to sell 1 lot 500CE for the hedge.

Now if PQR Ltd fall below 490, you can exit from your long equity at a loss of 10 rupee per share, at the same time you will gain ₹10 from the sold call options. Sometimes you may gain more than ₹10.

Secondly, If PQR Ltd hit your target of 530, the call options will expite at ₹30.00 and you will lose ₹7.00 where you will gain ₹30 from equity, an absolute gain of ₹23.00 will occur in your account.

Thirdly, if the stocks close at ₹500, they you will gain no money from equity but you will keep the premium of ₹23.00 for call writing.

In this example the call writing done for a moderate bullish or neutral view. Which may mislead as bearish outlook of the market. Opposite is also true for put options.

Another part, is options traders making Debit Spread strategy (May be Bull Call Spread or Bear Put Spread). In debit spread strategy, traders buy ITM options and at the same time they sell ATM options, now the Open Interest of the ATM options will increase and mislead common trader.

Now a days, OI data mostly mislead traders as many traders creating options strategies. OI data is effective only when you will use it with proper demand supply analysis context. My suggestion is before you start options trading you must acquire depth and proper nkowledge of technical analysis.

Put Call Ratio (PCR)

Put call ratio is another tools for options traders, which help them to understand the direction of the underluing. This never generate buy or sell signal themselves, but we can use it as a confirmation tools of price continuation or reversal with the demand supply context.

Open Interest Of A Put Option

Put Call Ratio= -----------------------------------------------------------------------

Open Interest of Same Strike Price Call Options

That means, we can say different strike price has different PCR, we have already discussed about Open Interest, I told you that, OI build up in Put options at demand refers the bullishness in price and OI build up at supply refers bearishness in price move expected.

When PCR of a particular strike price is greater than 1, is implies more put has been sold out than the same strike price call options, which indicates that traders have a bullish view on that strike price, or they are expecting that underlying price may get a demand near around the strike price. But this is the simpliest explanation, actually PCR study is more complex, in this study I have explained that complex part too in easy manner, read carefully the entire part.

For example, assume Nifty currently trading at 24800, now we saw the PCR of 24800strike is greater than 1. We can explain this as points below.

- Traders sold 24800PE more than they sold 24800CE.

- Traders expecting Nifty may not go below 24800 before expiry.

But in the above example I have explained with ATM options, what will happen if we go beyond ATM, let's learn practically.

Now assume 24500 Strike Price option's put call ratio is greater than 1, now this does not reffers bullish view in Nifty. Question is why?

Firstly, selling 24500PE is OTM, it reffers Nifty may not go below 24500 so I am selling 24500PE to get the time value as a profit, but at the same time some people have sold 24500CE which is deep in-the-money call options. When we sell a call options? Already I have told you that, we sell call options when we are bearish on that underlying, and selling deep in-the-money call options reffers strong bearis view.It means, if we try to understand direction based on PCR data then ATM options is the best choice along with demand supply context.

If we try to understand where the demand and supply lying, then we need to check the PCR in different manner. See the example below.

Assume Nifty trading 24800, now I am looking for where Nifty can get a supply or demand I will check multiple strike price open interest. I will check this below combination.

Traders sold 24800PE more than they sold 24800CE. Traders are expecting Nifty may not go below 24800 before expiry.

Traders expecting Nifty can take a bounce back around 24500 level. If currently price coming down.

But in the above example I have explained with ATM options, what will happen if we go beyond ATM, let's learn practically.

Now assume 24500 Strike Price option's put call ratio is greater than 1, now this does not refers bullish view in Nifty. Question is why?

Firstly, selling 24500PE is OTM, it refers Nifty may not go below 24500 so I am selling 24500PE to get the time value as a profit, but at the same time some people have sold 24500CE which is deep in-the-money call options. When we sell a call options? Already I have told you that, we sell call options when we are bearish on that underlying, and selling deep in-the-money call options refers strong bearish view. It means, if we try to understand direction based on PCR data then ATM options is the best choice along with demand supply context.

If we try to understand where the demand and supply lying, then we need to check the PCR in different manner. See the below example.

Assume Nifty trading 24800, now I am looking for where Nifty can get a supply or demand I will check multiple strike price open interest. I will check this below combination.

OI of Nifty 24750PE & 24850CE, 50 points far OTM from cmp.

OI of Nifty 24700PE & 24900CE, 100 points far OTM from cmp.

OI of Nifty 24650PE & 24950CE, 150 points far OTM from cmp.

OI of Nifty 24600PE & 25000CE, 200 points far OTM from cmp

I will continue in this manner. Now assume I found the open interest of 24600PE is 250000, where OI of 25000CE is 450000, here if we calculate the ratio it will be,

OI of 24600PE 250000

-------------------- = -------------- =0.55

OI of 25000CE 450000

It is referring that traders are selling 25000CE more than 24600PE, though both options are from the same difference from current market price. It clearly indicates that, traders expecting a sell-off if Nifty near around 25000, so 25000 is going to be a supply area.

Now imagine, both call and put options have almost equal open interest, then the question is what should be a trader's view? It indicates price will follow the prior trend. Almost equal OI may represent a PCR of 0.9 or 0.92 or 1.0 or 1.05 or 1.1 etc.

So if we say PCR>1 refers bullishness and PCR<1 mean bearishness, it will be an amateur trading view. My 21 years of practical experience saying until PCR>1.5 strong bullishness is not possible as directional trader of the options must ensure strong bullishness. Similarly I have noticed if the PCR<0.6 then strong bearishness appear in underlying price.

I have seen many traders to use PCR during expiry day. They choose same distance OTM call and put and compare OI data, and the best part they don't trade in every expiry day. They wait for either side 4 times OI build up on expiry day. For example on expiry day, nifty 300 point far OTM put option's OI=1000000, where 300 points far OTM call options OI=3000000 (Three times more than put OI) now the traders buy OTM put in Nifty at a cheap price, they expect a sudden fall before closing. I have seen then to get success several times, but personally I have never tried.

By the way, using PCR is complicated, if you do not know price action trading strategy in depth and may mess up your account with big losses.

Options Chain Analysis

Options chain analysis is another excellent tools for options traders, i it we many things about options like, options type (call options or put options), expiry date, strike price, options premium, open interest, implied volatility, and options greeks.

Different traders have different style to analyze options chain, here we will try to understand the future price movement of the underlying using options chain as well as try to understand the mass behaviour.

Firstly we will check the Premium, OI data & Implied Volatility of both ATM call and put options. Normally ATM call and Put options should have same premium. But practically if we see call options premium is at least 10% higher than put options, it refers that traders have bullish view on that underlying, and opposite is also true.

Secondly check the OI of in-the-money call and put options, if you found more OI in deep ITM call options, it refers that traders have a bearish view on that underlying and vise versa.

This is the trickiest part of options chain analysis. Open Interest build up in Deep in-The_money options series (not a single strike price but check a few strike) gives a clear view on future momentum. For example we can say if OI build up in deep ITM call options (at least 3 strike prices in a row) then it refers that the underlying may fall sharp from the current level and there are lots of potention of down fall and oppositely we can say if the OI increased significantly in Deep In-The-Money put options series then an immidiate significant up side movement we may expect. But the trickiest part is to identify significant OI build up in Deep ITM options. Unless you monitor the historical OI data of a particular expiry, you will never differentiate between normal OI and significant OI in deep ITM options.

There are no thumb rule of how much increase in OI can be called significant OI build up, therefore you must be familier with normal OI of any underlying options for a particular expiry. 1st July 2022 I had noticed OI of ICICIBANK 750PE was significantly increased, on 1st july 2022 ICICIBANK stock price closed at 703.9, that mean 750PE is far deep ITM put options. The OI of 750PE increased almost by 50% compare to previous days average OI, not only that but also volume was also increases dramatically. At the same time OI of several deep ITM also incresed dramatically including 800PE. I purchased equity after this to test whether the logic work perfectly or not, now you can see the chart after 1st July 2022 what ICICIBANK has done even in short term. After this I have successfully utilised this study in many of my personal trading.

Thirdly we will check implied volatility to understand how the options going to behave in near future, if implied volatility is low it means the underlying may tend to go up and accordingly we have to take action. If we see volatility is higher than expected, it refers an increase in options trading, traders are not sure about the continuation of the trend.

We will check Options Greeks for strike selection in case only long or short options. Strike Price selection is depnds on many factors, a depth knowledge of technical analysis and options trading require, however, intially we can use a shortcart for strike selection as explain below.

Strike Price Selection

Strike price selection is one of the most important part of options trading, specially for long call, long put, short call, short put trading

It depends on many things like stock price, expiry date, time value & intrinsic value etc.

Stock Price: If you buy far OTM options there are less probability you will able to make money if hold till expiry. So buyers should not focus to buy OTM options.

If you buy ATM options, still there are huge risk if you carry the position till the expiry unless a significant price movement in direction of your trade. Even an ATM options buyers may lose money if suddenly volatility drop in short term. So we can say buying ATM options is also a bad idea except trending market.

In case of ITM options, make sure the options has good volume, else it can create a problem during exit. Also make sure the ratio of Intrinsic Value & Time Value is minimum 3:1

In case of call options buying, make sure there is a demand near around your strike price, and in case of put buying, make sure there is a supply near your strike price. Remember here demand supply does not mean demand and supply zone, it may be any buying and selling pattern as per price action analysis.

In case selling an options, determine the demand supply first and select the strike price near to your stop loss for selling. For example if you find a PQR Ltd has a supply around 220-224 level and the striek difference is 5/- then sell 230CE not 225. Similarly you can select strike price of a put options also for shorting.

For options selling, depth knowledge of technical analysis and demand supply is mandatory as well as options terminology. As you will gain more experience in options trading you will learn yourself which ITM strike price to sell at what scenario.

Options Greeks

Options Greeks are tools to measure the risks involves in options trading, these help us to understand the different factors affecting options price (premium), calculated by using theoritical options pricing model.

Greeks are important because options behave and priced are relative to the one or more options greeks. This Greeks gives you deeper understanding of your risk. Greeks help you to structure more intelligent position.

There are five Options Greeks, Delta, Theta, Gamma, Vega & Roh

Delta

Delta is a measure of change in options premium for one unit change in the underlying price.

In India, we measure 10 points=1 unit in case of Nifty, Bank-Nifty and Fin-Nifty options

And 1 point=1 unit in case of stock options.

For call options, Delta has a range from 0 to +1 as the premium of the call options increase with the underlying price, and the Delta of a put options range from 0 to -1 as the premium of a put options negatively related to the underlying price.

For call option,

Delta of a Far OTM approaches 0.

Delta of an ATM approximately +0.5.

The more Deep ITM Call options, Delta approaches +1.

For put options,

Delta of far OTH approaches 0.

Delta of an ATM put approxmitely -0.5

The more Deep ITM Put options, Delta approaches -1

Delta has three main view,

- As a measure of change of option's value with respect to a change in the price of the underlying asset.

- As a hedge ratio.

- As an approximate probability of expiring ITM.

Let me explain with example..

Firstly, assume Delta of Nifty 24800CE =0.56, it means, if Nifty rises 10 point the premium of the call options will rise by 5.60/-, if Nifty fall by 10 point then the option premium will fall by 5.6/-

Secondly, if you have shorted Nifty future, then you can do a neutral hedge. Let's learn the calculation.

Assume you have shorted Nifty future at 24800, your stop loss is 25000. Now what you can do to hedge the position? You can buy call options. If Nifty rise, future will give you loss but options will give you profit. But if you buy ATM ot ITM call options, then it will be very tough to make profit. So you need to buy OTM call options. Which OTM and How many quantity?

If 25000 is the stop loss as per technical analysis then you shoud buy Nifty 25000CE to hedge your short position.

Now assume the Delta of 25000CE=0.27, currently lot size of Nifty future is 25, so multiply the Delta with Lot size to understand how many options you have to buy for the neutral hedge.

25*0.27=6.75

It means, if you have shorted 6.75 qty of Nifty then you should buy 1 lot 25000CE, so here you should buy 25/6.75=4 (Approximately) lots of Nifty 25000CE for the neutral hedge. Similarly we can calculate in case we have any long trade too.

Thirdly, If the Delta of Nifty 24800CE=0.56 it imples that, there are 56% probability that Nifty can close above 24800 and options will expire as ITM on expiration.

Theta

Theta measure the expected change in options premium for one unit change in time to expiry of the option. Theta is always negative for both call and put as the premium of the options goes down as the time to expiry decreases.

In other words, it give a view to the buyers of the options, how much value he will lose everyday if his view in not correct. Even if the underlying price is not changing but time decreasing, buyers of such underlying options will lose money as time value decay. This time value decay is measured by Theta.

For example, assume the Theta of Nifty 24800CE =22, it means, if means you are going to lose a time value of 22/- everyday from the options premium if Nifty become choppy, actually even if Nifty move up in favour of your direction, still you will lose 22/- time value but in the mean time Delta, Vega & Gamma will rise the options Intrinsic value, and therefore we do not realise the time value decay.

Gamma

Gamma measure the expected change in Delta for one unite change in the underlying, this mens as the underlying price changes, Delta of an options also changes, now the changed Delta is the expected change in the options premium for one unit change in the underlying price.

For example the Delta of Nifty 24800CE =0.56 and now Nifty currently trading at 24812, if Nifty reach 24822 then we will see the delta will also increase, it may be 0.58 or more. So we can say Delta of an options is not fixed, but it is varies with the underlying price.

This is why when there an one way movement in the underlying price, the premium of an options increades exponentially.

By the way, we need to remember, that the Gamma of an options is significantly higher when an options is near to it's expiry. So the writers of an options must closely watch their position when the options is very near to the expiry, a smal opposite direction can cause big loss for the options writes during this time. In other hand, this is the golden time for the options buyers for maximuze their return as the time value of the options is very minimum.

Vega

Vega measure the expected change in the options premium for one unit change in the volatility, Vega is always positive for both call and put as the premium of an options increases when the volatility increases and vise versa.

Remamber the price of an options is always remain discounted before the news comes in the open platform, you will notice one thing that, when there is an event, the Implied Volatility remain very high and before the event the premium of the options will also remain very high. It means the premium of the options already effected by Vega. Once the event will be over the options premium will fall dramatically as the Vega fall sharply.

So before an event trading options are too risky. Unless you gain more experience, building options strategy during events will be wise decision compared to only call or put options buying.

Roh

Roh measure the expected change in value of an options in respect of one unit change in interest rate. One unit change in interest rate means 100 Basis Point change in Repo rate. Which don't happen now and then. This is why we consider Roh as an insignificant options Greeks.